July 2023 Portfolio Construction

Stephen Lingard, SVP, Co-Head of Multi-Asset, CIGAM Portfolio Management.

Headline inflation has been the single biggest macro factor affecting financial markets over the past 18 months due to the resulting impact on global monetary policy. Central banks around the world have scurried to remove monetary accommodation by raising short-term policy rates at the fastest pace in decades.

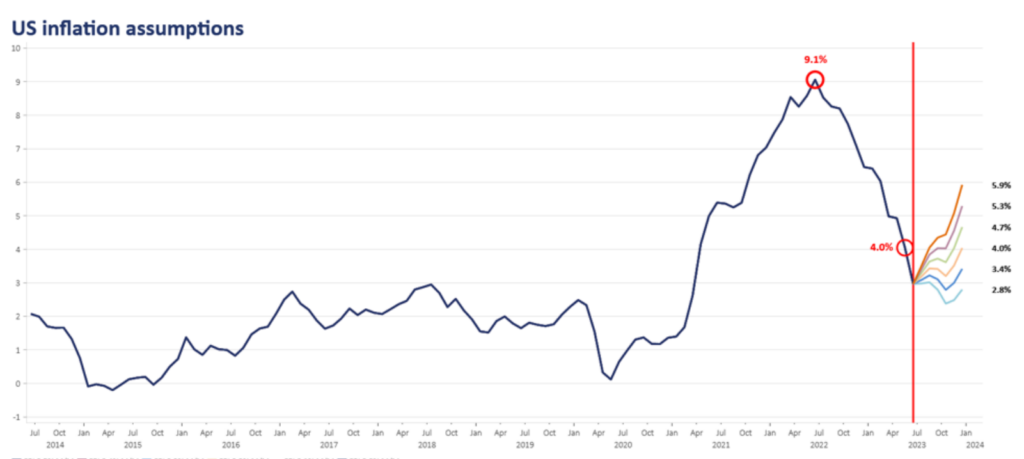

This has been done to avert a 1970s-style boom in inflation, which saw short-term interest rates become unhinged as they soared from 5% to nearly 15% by 1980. Such a rise in interest rates today would have a devastating impact on asset prices, so the June CPI number was a breath of fresh air as US inflation continued its decline towards target, falling to 3.0% year-over-year from 9.1% a year ago. However, the latest number was widely expected to be a good number due to base effects. This means that significant monthly inflation increases from over a year ago would be dropped from the calculation. Consider that in the first six months of 2022, the monthly CPI figure averaged 0.8% which represents close to 10% inflation on an annualized basis. Clearly, dropping this string of ugly monthly inflation numbers was critical to the recent fall in inflation to 3%. And what was principally behind this inflation surge in the first six months of 2022?

The devastating war in Ukraine, which saw the price of Brent crude almost double to a high of $130, subsequently boosting food inflation and pushing many related prices significantly higher. This was on top of the higher inflationary effects of supply chain disruptions caused by COVID-19, which are now believed to have mostly worked their way out of the monthly figures. The graph below highlights that because of base effects dropping out of the calculation, inflation is set to rise again in all but the most optimistic monthly inflation reports to come later this year.

Consider a range of monthly inflation numbers starting with 0.0% to 0.5% and see the projected impact for year-over-year inflation figures going into the end of this year and beyond.

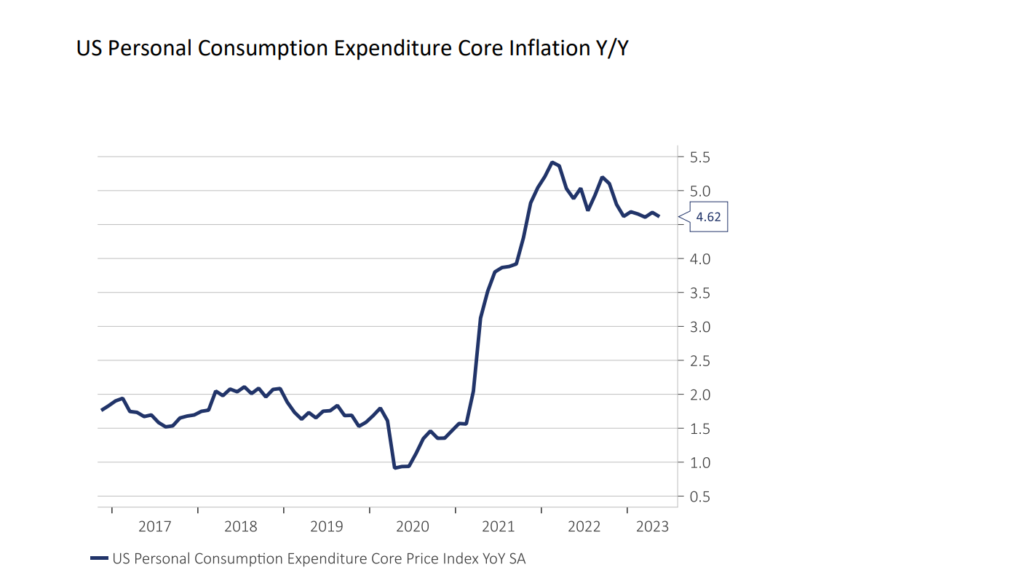

Core inflation, like US PCE, tends to be driven more by fluctuations in service inflation than goods inflation, so we need that part of the economy to slow. Service inflation tends to be tied to wages, so strong wage pressures in the economy currently suggest service inflation will take longer to roll over than the goods inflation which drove the significant improvement in headline inflation as it fell sharply over the past year. Slower wages are a function of the level of unemployment so, with the unemployment rate at historically low levels, the Fed will continue to try to weaken the labour market by slowing the level of economic growth. But keep in mind, the Fed has raised its overnight policy rate by 500 bps in a little over a year, which is extreme in terms of tightening speed. We will likely continue to see the lagged and variable effects of monetary policy on the economy and further significant increases are unlikely to be needed.

In terms of positioning, we are slightly underweight bonds as sticky inflation and resilient growth mean interest rates may stay high, disappointing investors looking for capital gains from fixed income. Meanwhile, higher inflation is likely to keep equity valuations in check while mounting pressure on corporate profit margins which have been falling as revenues fall faster than expenses. As such, cash is a tactical overweight for this stage of the cycle where stagflation (higher inflation, lower growth) is a higher-than-normal probability.

And so, inflation will continue to be an important issue at least into 2024, and possibly beyond. There is no doubt we have made significant progress on inflation, but it’s too early to declare victory.

We can help

We are here to help you meet your investment goals and we welcome your questions. We work with business professionals, executives, and families to grow and protect their wealth using our Wealth Plan formula. To discuss our approach and if it is the right fit for you, we invite you to schedule a no-obligation discovery consultation.